Who Buys Technology Companies and When?

Unless you plan to build a company over several decades, you should plan how your company will eventually exit. If you are not planning to take your company public, then you need to look for another company that will acquire you.

There are many types of acquirers for technology companies: companies of all sizes (not just the big ones); private equity (PE) and similar funds; family office investment funds; and entrepreneurs.

Acquirers generally can be categorized as strategic or financial according to their motivations in acquisition.

In general, strategic buyers are typically large or medium sized companies in the same or related technology space looking for synergies with the acquired company, as well as adding revenue and earnings.

Financial acquirers are typically less adventurous. They typically acquire private technology companies which have predictable revenues and earnings which are accretive to the acquiring company. Some acquirers, including large and small companies, family funds and entrepreneurs, are looking to manage the business over the long term.

Other acquirers, in particular private equity (PE) firms, want to add value over a shorter period. They may look to first acquire a large “platform” technology company and then “add on” smaller complementary businesses. The PE firm will increase earnings of the platform and add-ons over a 3 – 5 year period, and then sell the group at a profit.

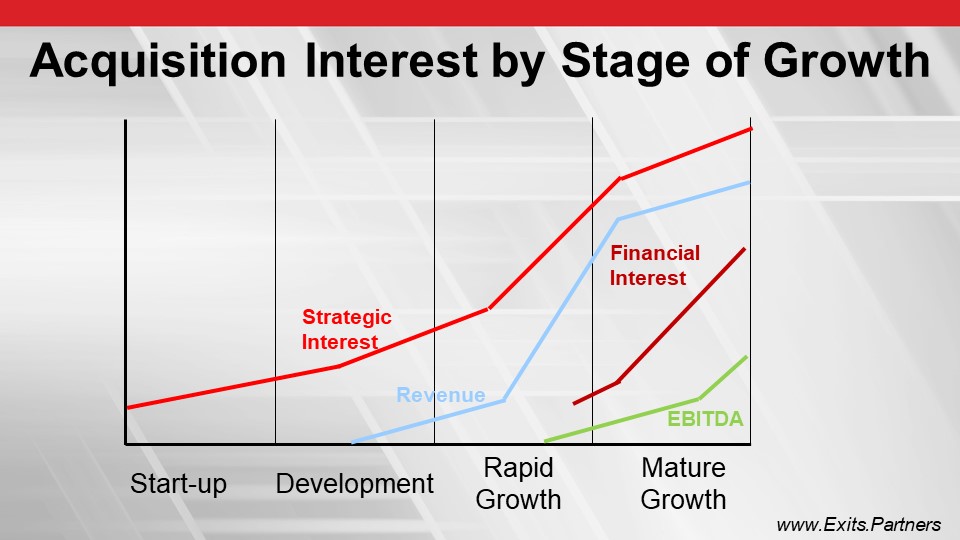

Strategic and Financial acquirers are interested in acquisition at different stages in the growth of a tech company. In the chart below, we have described four stages:

- Start-up: an individual or small group with an idea in development mode, little structure if any, pre-revenue and EBITDA

- Development: completing a version 1.0 and/or a first beta customer, company developing structure, some revenues from early adopters but not profitable yet

- Rapid Growth: more professional investment, product proven, sales accelerating, profitability in sight, company adopting formal structures and governance

- Mature Growth: company large and structured, sales growing predictably, company profitable

Link here to learn more about technology company development and governance.

The blue and green lines in the chart depict the growth of revenue and EBITDA, respectively, through the stages of growth. Revenues start in the Development stage and accelerate through Rapid Growth. EBITDA begins in Rapid Growth and grows from there.

The red and burgundy lines indicate where strategic and financial acquirers, respectively, become more interested in an acquisition through the stages.

Financial: Financial acquirers are all about the numbers. While they pay lip service to synergies in an acquisition, the reality is that every acquisition is done based on the accretion to earnings. They typically won’t look at a company until there is a track record of earnings near the end of the Rapid Growth stage, as shown by the green line. As the earnings grow and the company becomes more predictable in the Mature Growth phase, Financial acquirers become more interested.

By contrast, it is very difficult to interest a Financial acquirer in an early-stage tech company because the track record and profits are not yet there. Competitive advantage, strategic partnerships, killer apps, and the other elements that are critical to early-stage tech companies do not resonate with Financial buyers.

That said, with the amount of money available for acquisitions in the early 2020s, some PE firms are broadening their horizons and acquiring companies at much earlier stages than typical. If they wait until the company grows enough to meet their typical acquisition requirements, they may lose to a hungrier competitor, so they are buying companies earlier and at higher prices.

Strategics: the red line indicates that Strategic buyers may be interested in acquiring a tech company at any stage of its growth. Strategics value the synergy that the target company can bring with its technology, particularly if it is protected with solid patents. The Strategic buyer may acquire a tech company to accelerate their own product development and reduce the time to market. The strategic value to their business may be more important to an acquirer than their revenues and earnings.

That said, revenues and earnings are important. Many Strategics need to see all three components before they are interested, since there is no better validation of a new technology than happy customers.

In valuing a company to generate an acquisition offer, both Strategics and Financial acquirers tend to use multiples of revenue or EBITDA. See companion article: “Methods for Valuing Technology Companies”. A Financial acquirer will stick with its proven formulas. The Strategic buyer, however, may increase the multiple to account for the synergies.

If the Strategic buyer is interested in a company in the start-up stage with no meaningful revenue, the buyer will use non-financial, tangible metrics to form a valuation. These metrics may include the number and strength of patents; person-years invested in development; size and experience of the development team; development lead time over competitors; and, a comparison to companies at a similar stage of development.

Regardless of the stage of growth or the type of buyer, a company will maximize its valuation in an exit by engaging an experienced exit adviser. A well-planned and executed exit process can increase the exit value by 50% or more. In 2017, Strategic Exits sold a robotics start-up which had not yet completed product development, and therefore had no revenues, for more than $200 million.